Golar: Thinking Through the Downside

Background

Please see this Twitter thread of background on the situation:

I was initially skeptical of this situation given the investment history of large pieces of metal that float in water but after some researching I see the merits. These FLNG vessels are supposed to be cheaper and quicker to build than terrestrial based LNG facilities. Additionally, they are better suited towards stranded offshore gas assets. Therefore it seems possible that there will be demand for incremental facilities that GLNG can provide

Investment Thesis

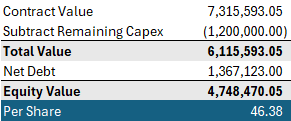

The most attractive part of the GLNG assets is the 20yr contractual cash flows each vessel has

I estimate that GLNG is selling below the present value of these cash flows alone leading me to believe there is very little fundamental downside at today’s prices

I get to ~$45 of DCF value for the current contracts

We are getting all the commodity exposure, inflation protections and growth potential from more vessels for free (the link above covers upside scenarios)

Risks

Risks are covered in the link above (counterparty risk and a cancelation of the 20yr contracts is by far the most problematic)

I am hoping that GLNG diversifies its counterparties to mitigate this risk

GLNG may also trade on South America and energy sentiment

Concluding Thoughts

I am not aware of many situations where you have clear downside protection from contractual cash flows and clear upside optionality / inflation protections

If anyone has any similar risk / rewards with clear downside protection, please share them! Id love to build a portfolio of businesses like these

The one holdback I have on this one is that the cash flow inflections will take years to materialize. Hopefully the stock trades up on newbuild announcements but if we are reliant on the vessels actually up and running it might take years

Bottom Line: This is a quick note where the primary point is to frame up the low risk and point out the free upside which I believe makes it a good r/r for the portfolio